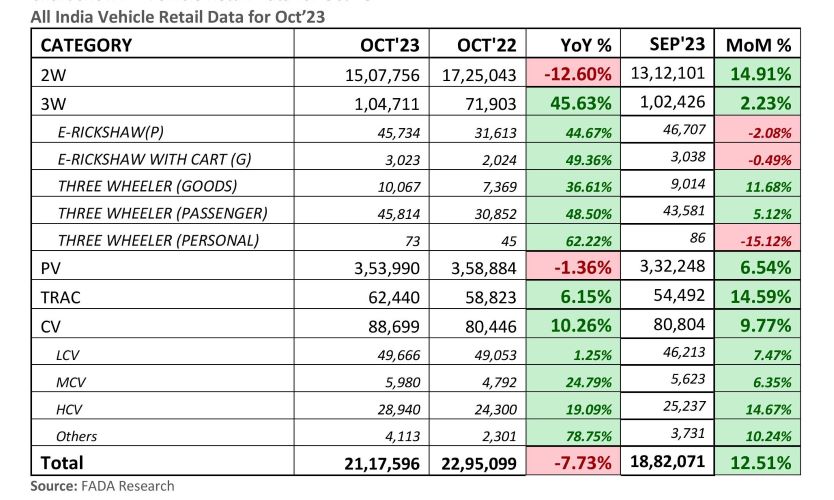

When compared MoM, Auto Retails flourished, achieving a 13% increase, with contributions from all categories. Two-wheelers, three-wheelers, passenger vehicles, tractors, and commercial vehicles expanded by 15%, 2%, 7%, 15%, and 10%, respectively, underscoring the sector’s robust growth momentum, according to the data released by the Federation of Automobile Dealers Associations (FADA).

The first half of October ’23, marked by the Shraddh period, saw an 8% YoY decline. However, a MoM comparison reveals a 13% surge, indicative of resilient market demand.

Commenting on October 2023 Auto Retails, FADA President, Mr. Manish Raj Singhania said, “The month commenced under the shadow of the inauspicious Shraddh period, persisting until the 14th. Consequently, a YoY comparison may not accurately reflect the actual trajectory of growth in the Indian Auto Retail sector.”

During the Navratri of 2023 retail sales soared by 18% year-over-year, surpassing the figures of Navratri 2017. Except for tractors, which saw an 8% decline, all categories exhibited commendable growth. Two-wheelers, three-wheelers, commercial vehicles, and passenger vehicles experienced increases of 22%, 43%, 9%, and 7%, respectively, FADA said in a media release.

The 2W category during the Navratri period and throughout October saw several positive trends, buoyed by festive cheer and stronger rural demand. Enhanced availability of models, especially those in high demand from the previous year, along with better financial schemes, contributed to a solid market momentum. States going into elections also injected optimism into the market, leading to an increase in government spending and improved liquidity. Despite a shift in festival dates, with Diwali moving to November, the anticipation of the festive season stimulated purchase intent and dealers reported good stock preparation and robust ground efforts that led to an uptick in sales figures, showcasing a resilient and adaptive market.

The 3W segment continued the uptick in demand during Navratri, largely driven by competitive finance options and a significant rise in e-Rickshaw interest, signalling a healthy move towards electrification. October continued this positive trend with robust market sentiments and festive celebrations contributing to increased customer bookings.

The CV segment experienced robust bookings and a positive uptake in retail sales, buoyed by festive cheer and strategic price support from manufacturers. The demand for light and small commercial vehicles surged, driven by infrastructure development activities and the need for vehicle replacement. Healthy demand was witnessed especially in segments like cement, iron ore and coal transport. The festive seasons, including Navratri, catalysed market activity, with customers taking advantage of favourable finance schemes.

Throughout the month, the anticipation for Diwali in November and the launch of new models generated a steady demand. The period overall saw a resilient PV market, supported by a stronger product line-up unlike last year, when stock availability was a major issue, the release said.

Near term outlook:

The near-term outlook for the auto sector is a blend of highs and lows as we approach year-end. Festivities along with harvest season (especially paddy) are expected to boost 2W sales, with optimism fuelled by new schemes and a push towards electrification, despite supply concerns. CV’s are looking at a strong November, with festive and construction activities enhancing demand, alongside anticipated financial schemes, FADA said.

However, the PV segment is navigating through a tricky phase. Festive days might spike bookings, yet the shadow of year-end discounts looms over immediate sales. High inventory levels in PVs, at a critical 63-66 days range, demand urgent attention from OEMs. Without substantial interventions and if Diwali sales don’t rise to the occasion, the weight of unsold stock could lead to significant dealer distress, echoing FADA’s concerns for potential industry-wide repercussions. Immediate and decisive action is imperative to counter the risk of a financial squeeze as the year closes.

Critical inventory concerns in PV segment: With passenger vehicle inventory levels soaring to an all-time high of 63-66 days, dealerships are signalling capacity concerns. FADA has issued a red flag, urging OEMs to not only moderate vehicle dispatches but also to introduce more aggressive and attractive schemes promptly. This dual approach is essential to help dealers clear their inventory before year-end, averting the potential financial repercussions associated with excess unsold stock, the release said.

Key Findings from Online Members Survey:

Average inventory for Passenger Vehicles ranges from 63-66 days; Average inventory for Two – Wheelers ranges from 40-45 days.

Liquidity: Good for 48.81%; Neutral for 39.29% and Bad for 11.90%. Sentiment: Good for 48.81%;Neutral for 41.67% and Bad for 09.52%.

Expectation for November: Growth for 55.95%; Flat for 37.30%, and de-growth for 06.75%.

{kind=link}