India’s automobile retail sector demonstrated remarkable resilience in May 2026, recording a 9.55% year-on-year (YoY) growth despite facing multiple headwinds, including a sharp fuel-price revision, extreme heatwave conditions, and ongoing geopolitical uncertainties in West Asia. According to the latest vehicle retail data released by the Federation of Automobile Dealers Associations (FADA), overall retail sales reached 25,31,067 units, making it the best-ever May performance for Passenger Vehicles (PV), Three-Wheelers (3W), Tractors, and overall vehicle registrations.

Passenger Vehicles emerged as the strongest-performing segment, driven largely by robust rural demand, while the growing adoption of alternative fuel technologies further accelerated market momentum.

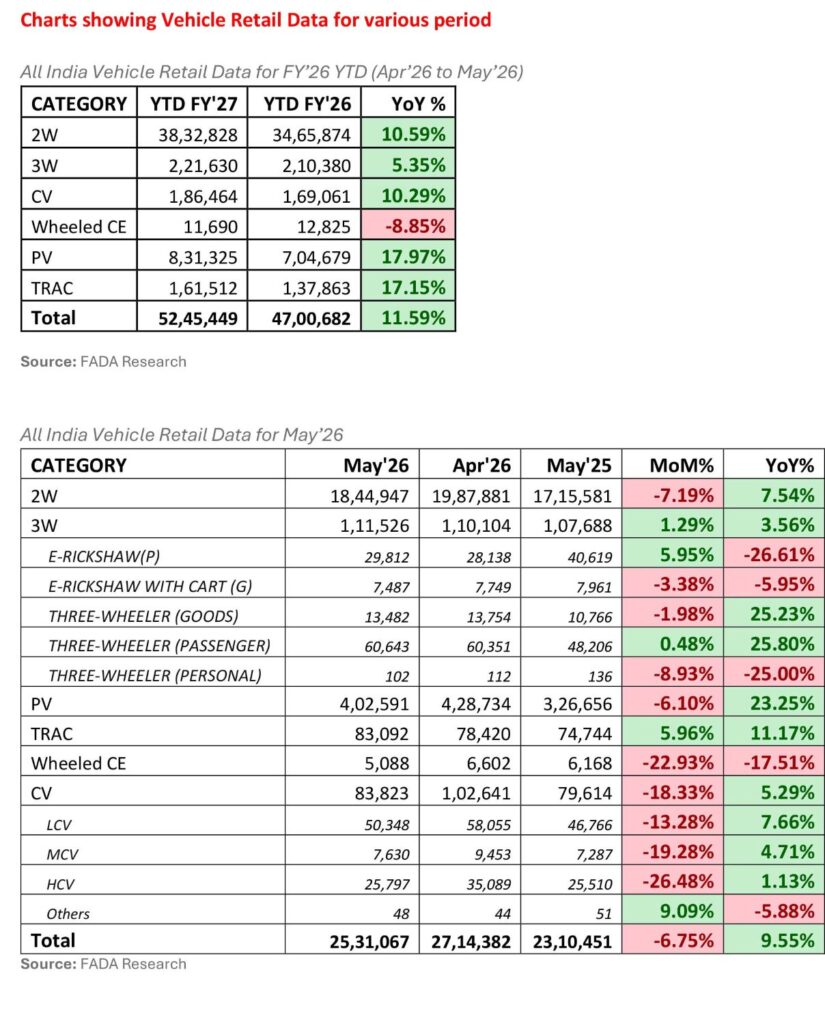

May 2026 Retail Performance

Total vehicle retail sales stood at 25,31,067 units, up 9.55% YoY. Segment-wise performance was as follows:

- Two-Wheelers: 18,44,947 units, up 7.54%

- Passenger Vehicles: 4,02,591 units, up 23.25%

- Commercial Vehicles: 83,823 units, up 5.29%

- Three-Wheelers: 1,11,526 units, up 3.56%

- Tractors: 83,092 units, up 11.17%

- Wheeled Construction Equipment: 5,088 units, down 17.51%

While retail volumes softened 6.75% month-on-month due to seasonal factors and delayed monsoon activity, the industry’s ability to sustain growth amid challenging market conditions highlighted the strength of underlying demand.

Bharat Drives Passenger Vehicle Growth

Passenger Vehicles delivered the standout performance of the month, growing 23.25% YoY to 4,02,591 units. Rural markets significantly outperformed urban regions, registering 30.35% growth compared to 18.80% in urban areas.

Dealers reported a revival in demand for small cars alongside continued preference for SUVs. Healthy booking pipelines, new product launches, and rising adoption of alternative fuel technologies also contributed to the segment’s strong performance.

PV CNG penetration increased to 23.34%, while EV penetration reached 6.63%, taking the overall alternative fuel share beyond 38% during the month.

Fuel Price Hike Accelerates Alternative Powertrain Adoption

The May fuel-price revision prompted a noticeable shift in consumer preferences toward fuel-efficient and alternative-powertrain vehicles.

Key penetration levels during May 2026 included:

- Two-Wheeler EV share: 9.25%

- Passenger Vehicle EV share: 6.63%

- Passenger Vehicle CNG share: 23.34%

- Commercial Vehicle EV share: 2.86%

The month also marked the highest-ever EV penetration across Passenger Vehicles, Commercial Vehicles and overall vehicle retail, with total EV share crossing the 11% mark for the first time.

Segment-Wise Performance

Two-Wheelers

Two-Wheeler retail sales increased 7.54% YoY to 18,44,947 units. Urban markets grew 11.75%, while rural markets registered 4.74% growth.

Marriage-season demand and affordability under the GST 2.0 framework supported sales, although heatwave conditions impacted showroom footfalls in several regions. Dealers also cited selective model-level supply constraints as a limiting factor.

Commercial Vehicles

Commercial Vehicle sales rose 5.29% YoY to 83,823 units, with rural demand outperforming urban markets.

Sub-segment performance included:

- Light Commercial Vehicles (LCV): +7.66%

- Medium Commercial Vehicles (MCV): +4.71%

- Heavy Commercial Vehicles (HCV): +1.13%

Steady freight movement, e-commerce logistics activity and replacement demand continued to support the segment, though dealers highlighted financing delays and rising freight and insurance costs linked to developments in West Asia as key concerns.

Tractors and Construction Equipment

Tractor sales grew 11.17% YoY on the back of healthy agricultural economics and positive rural sentiment.

Meanwhile, Wheeled Construction Equipment sales declined 17.51%, primarily due to a high base effect from the previous year.

Inventory Levels Require Monitoring

FADA noted that Passenger Vehicle inventory levels increased to 31–33 days at the end of May, compared with 28–30 days at the end of April.

The inventory level has now moved further away from FADA’s recommended benchmark of 21 days, prompting the association to urge OEMs to maintain disciplined dispatches during the seasonally softer June period to ensure inventory remains aligned with retail demand.

Commenting on the performance, FADA President, C S Vigneshwar, said: “Despite the challenges posed by an above-normal heatwave, fuel-price pressures and the evolving West Asia situation, Indian auto retail continued its growth trajectory. The industry achieved its best-ever May performance across Passenger Vehicles, Three-Wheelers, Tractors and overall registrations. The ability to sustain growth under such circumstances highlights the resilience of underlying demand across the country.”

June 2026 Outlook: Measured but Cautiously Optimistic

Dealer sentiment for June remains positive, with:

- 50.52% expecting growth

- 39.90% expecting stable demand

- Only 9.59% anticipating a decline

The onset of the southwest monsoon, early Kharif sowing activity, continued marriage-season demand and a stable financing environment following the RBI’s decision to maintain the repo rate at 5.25% are expected to support market activity.

However, elevated fuel prices, persistent heatwave conditions and developments in West Asia remain key risks to monitor.

Three-Month Outlook Strengthens

For the June–August 2026 period, dealer confidence has improved further, with 59.07% expecting growth.

Industry stakeholders believe advancing monsoon activity, stronger rural cash flows, Kharif sowing momentum and stable macroeconomic conditions will help drive demand recovery during the second quarter.

Supported by India’s strong FY26 GDP growth of 7.7%, policy continuity and improving rural sentiment, the industry is expected to transition from the current seasonal slowdown toward a firmer growth trajectory in the coming months.

Overall, FADA’s assessment for the next three months remains “Cautiously Optimistic,” with rural demand and monsoon-led economic activity expected to be the primary growth drivers.

{kind=link}